Understanding money topics, from saving and investing to protecting your income and planning for retirement, can make a real difference when it comes to building a financially secure future. But with so much information out there, it can be difficult to navigate these topics and know how to make the best decisions for you.

To find out how much Brits really know about money matters, we quizzed 2,000 people from across the UK on topics including ISAs, investing, insurance, income protection, and general personal finance. Through a series of 50 questions, we’ve revealed where there’s still room to grow when it comes to financial understanding.

We also delved deeper into some common misconceptions about finance topics, as well as what areas people feel the least confident in when it comes to managing their finances.

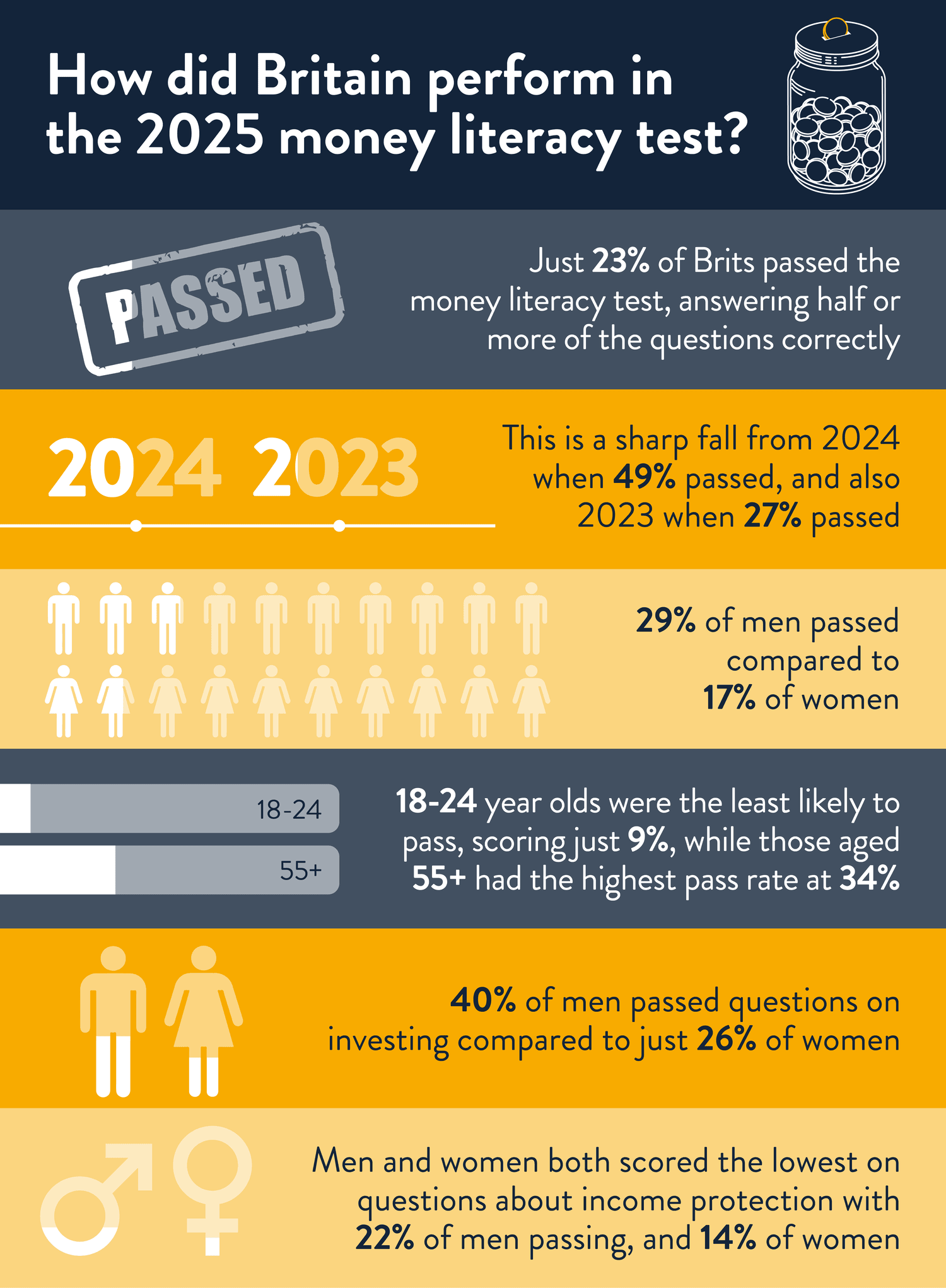

Under a quarter of Brits passed the money literacy test

This year’s results show a noticeable drop in financial knowledge across the UK. Our 2025 Money Literacy quiz found that only 23% of respondents passed, meaning fewer than one in four Brits answered at least half of the questions correctly. This marks a sharp fall from 49% in 2024 and is even lower than the 27% pass rate recorded in 2023, suggesting that financial understanding has slipped.

The breakdown of the results by age group shows that, as we’ve seen in previous years, financial literacy tends to improve with age. This year, only 9% of 18-24-year-olds passed the quiz, compared with 34% of those aged 55 and over. This trend is consistent with previous years: in 2023, 17% of 18-24-year-olds passed versus 35% of the 55+ group, and in 2024, 14% of young adults passed compared with 67% of older adults.

These pass rates show that younger people are still struggling to gain confidence and understanding when it comes to money. At the same time, financial literacy appears to be falling overall, with fewer people across all age groups passing the quiz compared to previous years.

| Age Group | Percentage that Passed | Percentage that Failed |

|---|---|---|

| 18-24 | 9% | 91% |

| 25-34 | 12% | 88% |

| 35-44 | 17% | 83% |

| 45-54 | 24% | 76% |

| 55+ | 34% | 66% |

Looking at the results by gender, men were more likely to pass the quiz than women, with 29% of men passing compared to 17% of women. This follows a similar pattern to previous years – in both 2023 and 2024, men also scored higher on financial literacy.

The biggest gap can be seen in questions about investing, where 40% of men passed this section of the quiz, compared to just 26% of women. Meanwhile, men and women both scored the lowest on questions about income protection with 22% of men and 14% of women getting half or more questions on this topic correct.

People in Nottingham are the most financially literate in the UK

Our research has found that residents in Nottingham are the most financially literate, with a third answering half or more of our questions correctly. Bristol came in second place, followed by Brighton in third.

At the other end of the scale, respondents in Leeds struggled the most with our quiz with just 15% getting half or more of our quiz questions correct. Leeds is followed by Belfast in second place and Cardiff in third.

Although some cities performed better than others, financial literacy challenges are evident nationwide, showing that the need for better financial education and guidance remains widespread across the UK.

The quiz revealed where the biggest gaps lie in our money literacy

When looking at the five key areas of personal finance covered in our 2025 quiz, income protection insurance was the topic Brits struggled with the most with only 18% of respondents passing this section. In comparison, pass rates were higher across other topics: 52% for general personal finance, 42% for insurance, 33% for investing, and 25% for ISAs.

| Topic | Percentage that Passed | Percentage that Failed |

|---|---|---|

| General personal finance | 52% | 48% |

| Insurance | 42% | 58% |

| Investing | 33% | 67% |

| ISAs | 25% | 75% |

| Income Protection | 18% | 82% |

Diversification and risk are misunderstood investment concepts for Brits

Turning the focus to investment, another area of the quiz where Brits struggled, we found that 27% believed that the past performance of an investment is a reliable indicator of future results. In reality, investment markets can fluctuate, and past success doesn’t guarantee future returns. Instead, investors should focus on long-term goals, keeping their investments diverse, and making sure the level of risk suits their personal comfort and circumstances.

When it comes to diversification, fewer than half of respondents (45%) knew that spreading your money across different types of investments, such as shares, bonds, and funds, can help reduce risk. Diversification means that if one investment performs poorly, others may help balance things out, making your overall portfolio more stable.

Despite this, many people still hold their investments in just one place or rely on a single type of product. At Shepherds Friendly, we offer an Investment ISA, which can be a simple and tax-efficient way to start investing. It could also be a great option to add to an investment portfolio.

Knowledge on ISAs has dropped compared to previous years

Comparing this year’s results to previous years, it’s clear that understanding of ISAs has slipped. In 2023, 34% of people passed the ISA section of our quiz, rising to 44% in 2024. But in 2025, that number has dropped to just 25%.

Only 32% of people knew that money paid into a Junior ISA doesn’t count towards an adult’s annual ISA allowance. This means you can save up to £9,000 into a Junior ISA each tax year, completely tax-free. This low awareness suggests that parents and guardians may be missing out on opportunities to make the most of this tax-efficient savings option to help prepare their children for the future.

Another common misconception is around the adult ISA allowance, which is currently set at £20,000 per tax year. Around 26% of respondents thought that any unused allowance could be carried over to the next financial year, but in fact, it cannot. If you’re able to, utilising as much of your ISA allowance as possible each year can help you make the most of tax-free savings and investment opportunities, helping you on the path to achieving any long-term savings goals.

Almost a third (30%) also believed that interest earned within an ISA counts towards your Personal Savings Allowance. Your Personal Savings Allowance is the amount of savings interest you can earn tax-free each year, which is currently up to £1,000 for basic rate taxpayers. This misunderstanding highlights a broader knowledge gap about the tax advantages of ISAs and how they differ from regular savings accounts, meaning some people might be missing out on fully maximising their savings.

Misunderstandings around income protection leave many Brits unprepared

Looking more closely at the questions that caught people out, nearly a quarter (23%) of respondents believed that self-employed people aren’t eligible for income protection.

In fact, they absolutely are. Since self-employed workers don’t receive sick pay from an employer, having income protection in place can be especially valuable, to help cover lost income if illness or injury stops them from working. For self-employed workers, Shepherds Friendly’s Income Protection policy can cover up to 70% of the average of their last three years’ net profit.

Meanwhile, 28% of people also thought that income protection only covers absence from work as a result of illness or injury for a period of six months. However, income protection can actually cover you for much longer, depending on your plan. In comparison, Statutory Sick Pay only covers you for up to 28 weeks during one period of sickness or injury, which might not be enough to cover what you need.

We recently conducted a separate study that delves further into Brits’ understanding of income protection, revealing that many are prevented from taking out this important policy due to misconceptions about who needs it, with some believing they don’t earn enough, are too healthy to need it. In reality, income protection can provide crucial financial support for anyone who relies on their income but is unable to work due to illness or injury.

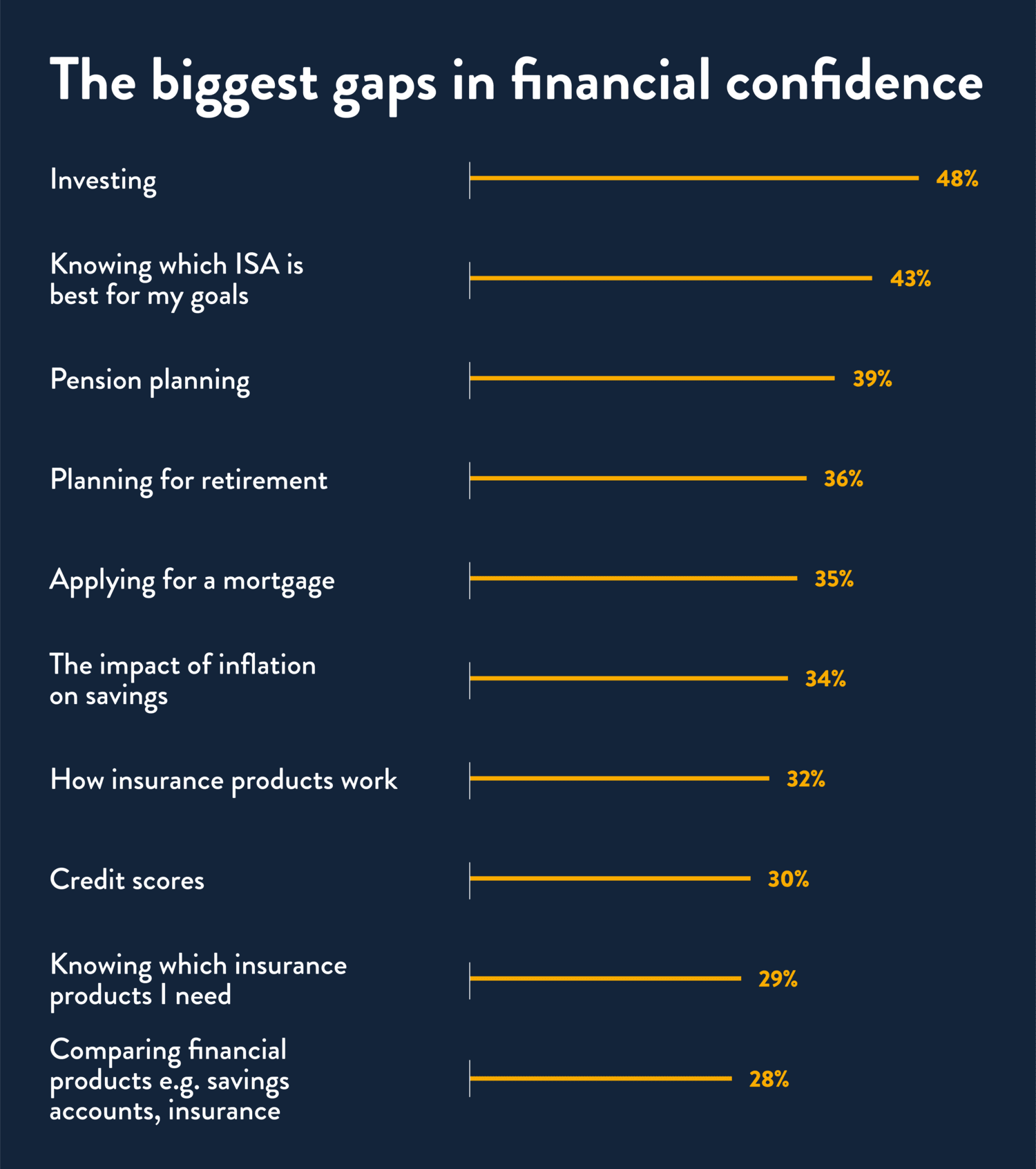

Brits are the least confident with investing, ISA savings, and pension planning

Asking adults how confident they are about different areas of personal finance, investing came out on top (48% not confident), followed by choosing the right ISA for their goals (43%) and planning for retirement (39%).

There were also noticeable differences between men and women. 60% of women said they don’t feel confident investing, compared with 35% of men. Similar gaps appeared for ISAs (52% of women vs 32% of men) and pension planning (48% of women vs 29% of men), suggesting that women may feel less equipped or less engaged when it comes to long-term financial planning.

Financial confidence gaps exist across generations

While younger people report the lowest confidence with financial topics, the survey also shows that older generations have gaps in their knowledge

Among 18-24 year olds, more than half said they aren’t confident in choosing the right ISA (55%), understanding pension planning (56%), or how insurance products work (53%). Worryingly, 47% also said they aren’t confident in their knowledge of the impact of inflation on their savings, which could mean many in this age group might not be taking steps to protect or grow their savings effectively.

Older adults generally feel more confident about finance topics overall, but uncertainty isn’t limited to younger people. More than a third (39%) of those aged 55 and over still say they don’t feel confident with pension planning, even though they are the closest age group to retirement in the survey. This suggests that confusion around finance topics isn’t just an issue for younger generations, but a challenge faced by many across generations.

70% of Brits call for finance topics to be taught in schools

Our results show there are still significant knowledge gaps among Brits, particularly among younger adults. With limited financial education in schools, many people are entering adulthood unsure about how to budget, save, or plan for their future.

A strong majority of Brits believe money literacy should start in the classroom. Seven in ten (70%) think personal finance should be part of the school curriculum, and 72% say students should specifically be taught how to save and invest, highlighting a clear demand for early education in practical money skills.

Missing early financial education may be harming money confidence

Our data also suggests that missing this early education has real consequences. Among 25-34-year-olds, 51% say they are struggling to manage their money amidst rising costs, compared with 40% of the population overall. This age group also reports the highest levels of financial stress, with 46% saying they’ve lost sleep over money, and 55% admitting that financial worries have negatively affected their mental health.

Financial preparedness is also low across all age groups. Over a third (34%) of Brits don’t feel they know enough to handle a financial emergency, while 35% say they aren’t financially prepared if one were to happen. Even more concerning, only 54% regularly review their financial goals, and just over three in 10 (34%) feel confident they’ll achieve them, suggesting that many people may be missing out on opportunities to grow their savings and plan effectively for the future.

These findings highlight a clear opportunity: better financial education could help bridge these gaps, giving young people and adults alike the tools to budget, save, and invest wisely. By improving money confidence early, we could reduce stress, prevent future financial regrets, and build a stronger foundation for long-term financial wellbeing across the UK.

Derence Lee, Chief Finance Officer at Shepherds Friendly says: “Our survey shows that many people feel unsure about different areas of personal finance, from investing to insurance. But understanding key financial topics and the products that can help plan for the future is essential for feeling confident when making decisions about your money. Improving financial literacy can benefit everyone, whether you’re just starting out or already thinking about retirement.

“Improving financial literacy doesn’t have to be complicated. You can start by familiarising yourself with key concepts like saving, investing, pensions, and insurance. Tools such as budgeting apps, online calculators, and interactive guides can make learning hands-on and practical. Reading trusted resources, following reputable financial blogs, or attending webinars can help build knowledge over time.

“For more personalised guidance, speaking to a qualified financial adviser can help you understand your options and make informed decisions tailored to your circumstances. Even small, consistent steps can build confidence and help you feel more in control of your financial future.

“There’s also a responsibility on providers of financial products to make their offerings easy to understand. At Shepherds Friendly, we aim to communicate clearly and simply, to help people understand our products and make informed financial decisions. By improving financial knowledge, we can all make smarter decisions, feel more confident, and build a stronger financial future for ourselves and our families.”

If you’re looking for ways to improve your financial literacy, head to the Resources section of our website, where you’ll find helpful information on a range of topics, from ISAs to insurance, as well as savings guides and practical how-tos.

Methodology

We surveyed 2,001 Brits aged 18 and over on their knowledge of finance topics. The research was conducted between 03/09/2025 and 08/09/2025.

The pass rate of the quiz was calculated by finding the percentage of respondents who got half or more of the quiz questions on ISAs, investing, income protection, insurance and personal finance correct.

Please note that year-on-year comparisons of the Money Literacy Quiz pass rate have been made in this blog post (from 2023, 2024 and 2025), however the quiz questions are not identical year-on-year. The aim is to measure overall financial literacy rather than exact question-level comparability.

When investing, your capital is at risk and you may get back less that you have put in. The payout from your insurance policy may be less than what you have paid in. If premium payments are not kept up to date your policy may be cancelled. ISA tax rules depend on individual circumstances and may change in the future.