Since they were introduced in 1999, Individual Savings Accounts (ISAs) have become one of the most popular ways to save. ISAs are exempt from income tax and capital gains tax on the investment returns, and you also don’t pay any tax on money withdrawn from your ISA.

Government figures show that around 12.7 million adults subscribed to an ISA in the tax year 2015/16, and 740,000 Junior ISA accounts received contributions in the same period.

There are limits to the amount that you can save into the different types of ISA, and these limits are reviewed by the government every year. Keep reading to find out what the ISA allowances are in the 2018/19 tax year.

Related: What are the 2019/20 ISA allowances?

Cash and Stocks and Shares ISA

Each year, your ISA allowance resets. This means that you can invest up to a certain amount in your ISA every tax year. You cannot carry your ISA allowance over between tax years, so if you don’t use it you lose it.

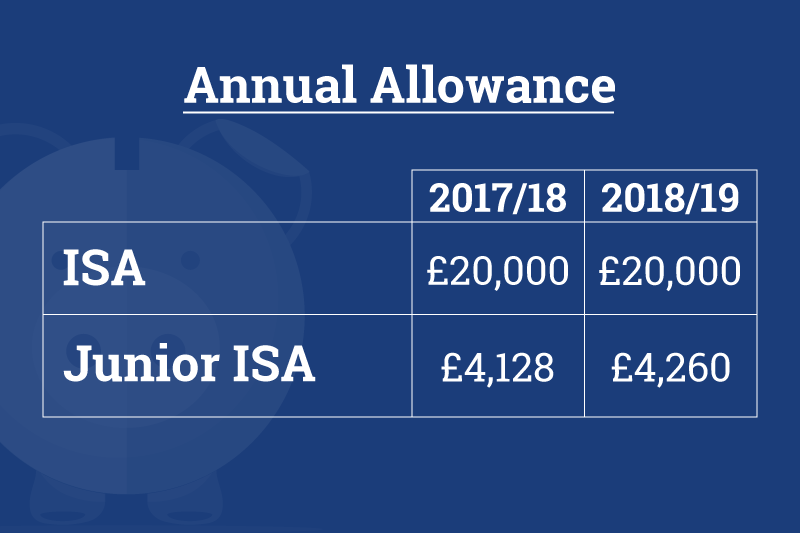

Last year the main ISA limit was increased from £15,240 to £20,000. In the 2018/19 tax year the ISA savings limit will be frozen at £20,000.

You can split your ISA allowance across a Stocks & Shares ISA and Cash ISA or invest it all in either one. You can either invest lump sums or you can save on a regular basis. For example, our Stocks and Shares ISA lets you invest a lump sum of between £500 and £20,000, when opening and you can then invest lump sums starting from £100 as and when you wish, or you can save on a monthly basis from at least £30 every month.

Junior ISA

Junior ISAs are a tax-efficient way of building up a nest egg for your child’s future. They let you provide your child with a tax-free lump sum when they reach the age of 18.

The annual subscription limit for Junior ISAs for 2018/19 will increase in line with inflation, from £4,128 to £4,260.

Many Junior ISAs let you save through lump sums or regular payments. Our Junior ISA accepts monthly payments starting at £10 as well as one-off payments of at least £100 when opening then £10 thereafter. In the 2018/19 tax year you can save up to £355 per month.

From age 16 a child can also have an adult cash ISA alongside their Junior ISA. They can still only save £4,260 per tax year in the Junior ISA, but they could also save up to £20,000 extra in an adult cash ISA between age 16 and 18.

The child can take control of a Junior ISA when they’re 16, but can’t withdraw the money until they turn 18.

Help to Buy ISA

Help to Buy ISAs were introduced 2015 to help first-time buyers to save the deposit for a mortgage. As well as tax-free returns, if you manage to save a minimum of £1,600 you’ll be entitled to an additional 25% bonus from the government.

In the 2018/19 tax year you can save an initial deposit of up to £1,200, and up to £200 a month. If you miss a monthly payment you cannot make up for it the following month.

Remember that rather than having one Help to Buy ISA per home, it’s one per person. If you’re buying jointly, as long as both of you are both first-buyers you can both take advantage of a Help to Buy ISA, including the bonus.

Lifetime ISA

Launched in April 2017, the Lifetime ISA allows you to save tax-free for a property deposit and for retirement. However, the Lifetime ISA can only be opened by those who are aged 18-to-39 years-old and you can save until you’re 50-years-old.

Savers can put in up to £4,000 each year until the age of 50 and the government adds a 25% bonus to the savings, up to a maximum of £1,000 annually.

There is no maximum monthly contribution and you can save as little or as much as you want each month providing you don’t exceed the £4,000 a year limit.

Note that the Lifetime ISA limit forms part of your overall £20,000 ISA limit.